Scoring Companies' Impact on UN SDGs

Scoring Companies' Impact on UN SDGs

This week we look at Robeco's open-data SDG scoring framework

The UN Sustainable Development Goals (SDGs) are a collection of 17 global goals that aim to end poverty, reduce inequality, and address climate change (among others) by 2030. These goals set specific targets and indicators to measure progress towards sustainable development.

The SDGs are important for sustainable investors as they provide a comprehensive framework for identifying and addressing both ESG risks and opportunities.

A popular example of applying the SDGs in investment can involve investing in renewable energy projects that align with SDG 7: Affordable and Clean Energy. Or supporting companies that promote gender equality in line with SDG 5: Gender Equality.

Investors can also integrate the SDGs into their due diligence process, engagement activities and reporting to demonstrate their commitment to sustainable development.

This week, we will look at how Dutch investment company Robeco measures companies’ SDG scores.

What is remarkable is the company has made the data open for public access. You can check out this link to find individual company SDG scores.

The database covers over 2,900 constituents in the MSCI All Country World Index so this is a good coverage of both developed and emerging market stocks.

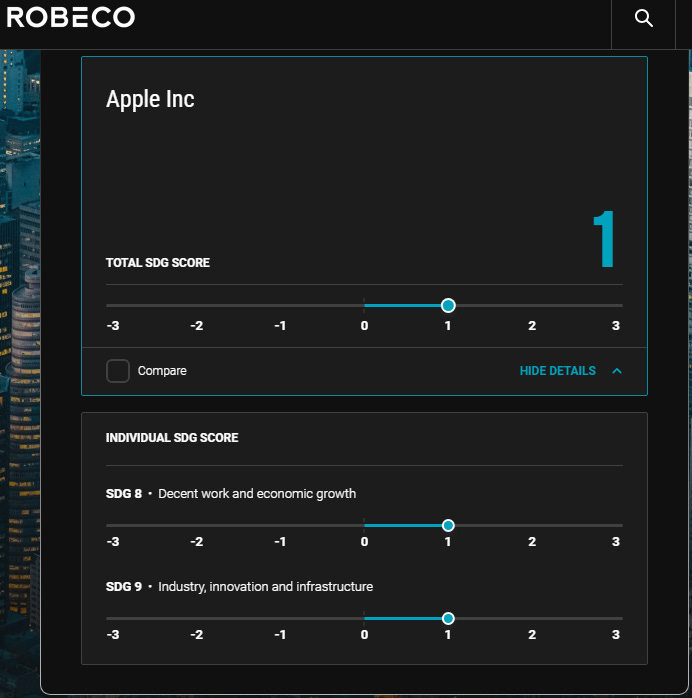

Using Apple as an example, we see the company scored a 1 for its Total SDG score on a scale from -3 to +3.

Looking at the breakdown of the score, Apple is rated in two components: its positive contribution to SDG 8: Decent work and economic growth and SDG 9: Industry, Innovation and Infrastructure, both with a score of 1.

As with all scoring frameworks, there is bound to be a degree of subjectivity. For instance, one could argue that Apple is a pretty innovative company and promotes sustainable industrialization, so shouldn’t it score higher than just a 1?

To answer this question and more, we will take a deeper dive into Robeco’s scoring methodology.

Let’s begin!

Three-step process

The assessment is split into a three-step process: Product, Procedure and Controversies.

Product

The first step is to determine the what. What does the company produce? Products that are considered to have a positive contribution to the SDGs would be goods like medicine, water or healthcare. On the other end of the spectrum, sin stocks like the ones in alcohol and gambling are likely to get a negative score.

In addition, there are also performance indicators to help gauge how well a company does in meeting SDGs. For example, a bank would have to generate more than or equal to 15% of its revenue from microloans to score a +2 in meeting the SDG 1: No Poverty (item 3 below):

Procedure

Step two is the how. The focus here would be more on a company’s sustainability impact. For instance, does a company dump waste irresponsibly? How is their board diversity?

Controversies

The last step focuses on the negatives. Simply put, if a company is involved in a legal dispute or a controversy, Robeco analysts would further scrutinize if the incident has had an adverse impact and what mitigating steps are taken.

Following these steps, companies’ impacts on each of the 17 SDGs are scored from a range of -3 to +3. How is the overall score then determined?

Deriving total score

Robeco uses a min-max rule, which states that if a company does not have any negative score (-1,-2,-3) on any of the SDG goals, it will be assigned the highest available individual score. Conversely, the company will receive the lowest individual score as its total score.

For example, Microsoft received 2’s for SDGs 8 and 9 and a 1 for SDG 5. Because it did not receive a negative score for any of the SDGs, its total SDG score is the highest available, which is a 2:

On the other end of the spectrum, we look at Vale, which scores a -3 on a few of the SDGs. Using the min-max rule, the company is therefore given the worst available individual score (-3) for its total score:

Not all SDGs are equal

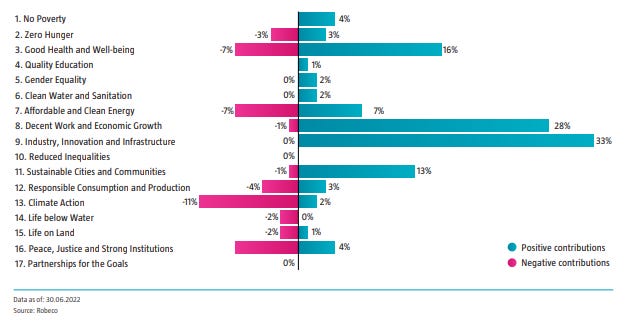

Out of the 17 SDGs, some are arguably easier to evaluate than the others. From the chart above, we can see most companies are graded on SDGs 9, 8 and 3.

SDG 10: Reduced Inequalities and SDG 17: Partnerships for the Goals, on the other hand, are probably more difficult to grade, as we see most companies do not have either positive or negative contributions in these. This again speaks to the inevitable subjectivity dimension here. After all, these are broad-based goals set by the UN and there is really no uniform way to measure progress.

Another way to look at SDG score break-down would be through industries.

Not surprisingly, companies in the energy sector have more negatives than the others, since their products are not likely to actively promote any SDGs.

Companies in Financials and Health Care have more positives, as these companies are in the “right” sectors that are more aligned with promoting SDGs, such as SDG 3: Good Health and Well-being.

As with any other type of ESG scoring, there is a sector bias here so blindly ranking stocks with high SDG scores will get you a portfolio full of IT, Industrials, Financials and Health Care stocks.

Using SDG scores

Robeco uses these SDG scores as a tool in their investment process, for instance by excluding companies with negative scores. They published a couple of papers (such as one here) that show that excluding these companies “is not expected to affect factor premiums”.

Another dimension of using the SDG scores is to customize a portfolio to tilt toward certain themes. For instance, a health-focused funds may choose to overweight companies that score high in SDG 3: Good Health and Wellbeing.

As we saw earlier, even with attempts to quantify the impact of SDGs using indicators or thresholds, subjectivity often comes into play. Therefore, it may not be very useful to spend time analyzing why a company like Apple receives a score of +1 instead of +2.

Besides that, there is also the issue of certain sector bias; companies in certain sectors (such as Energy) are just not going to score well for certain SDGs. While Robeco’s paper says that excluding negative scoring companies is not expected to affect factor premiums, there is also no evidence that picking companies that contribute to SDGs can help to outperform.

That being said, if you are an investor who cares about the SDGs, Robeco’s framework is perhaps the most systematic way to quantify companies’ impact at a large scale.

According to their methodology document, there are close to 70 sustainability analysts that create and maintain these scores for over 1,500 companies. Individual investors probably won’t have the time or resources to create their own SDG scoring framework.

The best part of this is that these scores are available to the public through their open data initiative. So, for individual investors who do care about SDGs, the best way to utilize this would probably be to use the scores as a tool to check their portfolio companies’ SDG scores and perhaps start engaging or selling those that rank poorly.